[ad_1]

[ad_1]

It’s comprehensible why many younger folks don’t make investments: They’d slightly use their cash elsewhere, or they may not suppose they've any additional money obtainable for investing.

However investing in your 20s is a golden alternative to construct wealth, particularly should you embrace the best degree of danger with the understanding that point is in your facet.

Final month, former monetary skilled and present private finance persona Mark Palmer posted on X (formerly Twitter), "If I used to be 20 years outdated proper now, here's what I might be investing in ..." The put up obtained practically 160,000 views, however extra importantly, it reignited the dialog about how and why younger folks ought to be investing — and the way and why their portfolio allocations ought to be totally different than older generations.

Palmer's listing of theoretical investments included some high-risk propositions, similar to placing 10% into bitcoin and one other 10% in individual stocks that he has "a variety of conviction in," together with bigger chunks in exchange-traded funds (ETFs). He acknowledged that "everyone seems to be totally different," and "what works for me could not be just right for you."

No matter whether or not you agree together with his particular choices, the overall thesis is one price contemplating, particularly should you're younger: Diversify, concentrate on development investments, and do not shrink back from danger.

Younger buyers: Larger danger is OK

Larger danger can lead to higher reward. However it may possibly additionally contribute to higher losses, not less than within the quick time period. That is why typical knowledge says buyers ought to start adjusting their holdings as they strategy retirement to scale back danger publicity and shield capital with extra conservative belongings like CDs and Treasury bonds.

Nevertheless, for 20-somethings, the alternative holds true. That cohort ought to be embracing "risk-on" methods as their funding timelines allow extra room for extra restoration. Meaning embracing greater danger asset lessons like shares versus safety-oriented belongings like bonds. Going a step additional, it additionally implies specializing in development shares versus worth shares. Whereas the latter are sometimes regular, dependable dividend-paying belongings, the previous routinely see extra upside potential.

In keeping with Invoice Van Sant, a licensed monetary planner who's govt vp and managing director at Girard, a Univest Wealth Division, youthful buyers' danger tolerance ought to be a lot greater, whether or not meaning particular person shares or funds slanted in the direction of aggressive development. "You merely choose a development fund, 100% equities, inventory. There isn't any taking a look at bonds or fastened earnings at that age."

Gen Z is already demonstrating a propensity for greater danger belongings. Knowledge from on-line funding platform Saxo reveals that amongst younger buyers, 60% personal shares and 54% personal crypto.

The extra diversified strategy is to place cash in ETFs with broad publicity to large-cap development firms. The Schwab US Massive-Cap Development ETF, for instance, gives entry to Microsoft, Apple, Nvidia, Amazon, Meta, Alphabet, Eli Lilly and Broadcom multi functional fund with a low expense ratio and with out having to personal every inventory individually.

As for these expense ratios or administration charges, Van Sant says, "Buyers ought to take note of bills, however do not let that fully devour or derail the funding ... Focus in your actual return after taxes and inflation."

When factoring for actual returns, the expansion potential of a portfolio composed of equities (shares, ETFs and mutual funds) can carry out higher for a youthful investor than conventional, conservative portfolio allocations just like the 70/30 or 60/40 models, that are cut up between equities and glued earnings belongings like CDs and bonds.

Begin investing for retirement now

A January 2024 ballot carried out by Northwestern Mutual discovered that People now imagine they're going to want $1.46 million to have a cushty retirement. The issue, nevertheless, is 50% of ladies and 47% of males between the ages of 55 and 66 have no retirement savings in any respect, in line with U.S. Census Bureau information.

Van Sant says that getting began on a path to retirement now could be the important thing to being ready later, even when it is the one investing 20-somethings can decide to.

"The primary factor to do is enroll in a retirement plan. Nearly all of employers have them now, and also you begin at 10% [contribution]. Your funds will adapt," he says. "Belief the method. Retirement financial savings is a marathon, not a dash."

One the most important benefits of collaborating in an outlined contribution plan like a 401(k) is getting access to an employer's match, which is akin to free cash. Like worker contributions, an employer match is cash added on a pre-tax foundation. On common, firms will match greenback for greenback contributions from 4% to six% of a employee's pre-tax compensation, as much as a specific amount.

Should you're unable to commit 10% of your wage out of the gate to a retirement plan, attempt to not less than put apart the utmost employer match quantity to get the ball rolling.

Van Sant additionally stresses the significance of accelerating contributions when it is financially possible. "Give your self a retirement elevate every year when your pay will increase or when you'll be able to afford it," he suggests, even "if that is solely a 1% enhance" out of your present contribution.

For many who do not have entry to an employer-sponsored plan, a tax-advantaged Roth IRA or self-employed retirement plan could be equally efficient. The necessary half is simply getting began. Van Sant says youthful generations are exhibiting indicators of being "extra saving-conscious" partly as a result of they're conscious of what can go fallacious if they are not ready for retirement.

"You see grandparents going again to work now. That resonates. The largest problem to retirees is longevity danger," says Van Sant. "The youthful technology has extra appreciation for that."

Embrace the facility of compound curiosity

Whereas older People are fretting about how far their cash will stretch in retirement, many members of Gen Z — these born between 1997 and 2012 — are preoccupied with determining their profession paths and whether or not or not they're going to ever be capable of afford a home.

Regardless of information exhibiting youthful generations doing a greater job with saving for retirement and investing in comparison with older generations once they have been the identical age, the common age for folks right now to start investing is 34 years outdated, in line with the Monetary Occasions. Meaning Gen Z could possibly be doing extra as an entire whereas embracing methods that make sense given their age.

Compound interest can have an unbelievable impact on investments, however getting began early is important. The common investor getting their begin at age 34 is lacking out on a decade or extra of compounding that might in any other case have an outsized affect on their portfolio's development.

"Should you began 10 years earlier if you're 24," says Van Sant, "you do not have to place in practically as a lot to get to the identical end-dollar purpose ... the later your begin, the extra you must play catch-up."

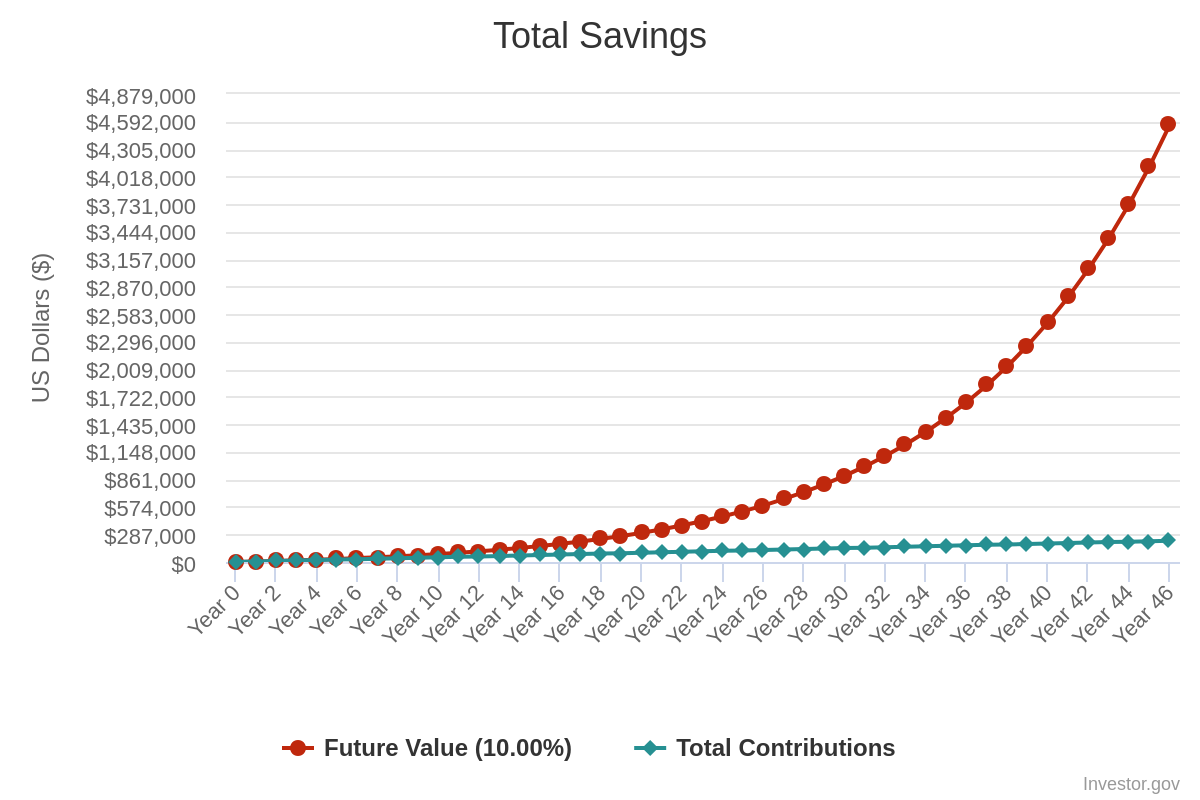

Utilizing his age 24 instance, say a first-time investor funded a Roth IRA with $1,000 and bought shares of an index fund with a historic common return of 10%. With a further $100 contributed weekly for the following 46 years — at which level they're going to be 70 — the whole contributed would complete $221,800.

Nevertheless, that retirement account would then be price $4.55 million with out taking dividends into consideration, which most index funds pay quarterly and could be robotically reinvested into positions.

That is the facility of compound curiosity. However that payoff hinges on getting began prior to later, as a result of delaying that call means misplaced alternative.

As Van Sant places it, "An investor's greatest good friend is time."

Extra from Cash:

Why the Recent Rise in Stock Buybacks Is a Good Sign for Investors