[ad_1]

[ad_1]

Buying a house is much more sophisticated than swapping money for a set of keys — along with residence inspection charges and an preliminary deposit, there’s a laundry listing of prices homebuyers should pay earlier than transferring in.

Among the many largest? The down cost.

Typically, the extra you possibly can pay upfront, the decrease your month-to-month mortgage invoice will probably be. Most residence loans require a minimal down cost of three% of the sale value, however 20% is historically thought-about perfect by mortgage lenders.

These days, which may be simpler mentioned than accomplished. U.S. residence costs have climbed to new heights since 2020’s pandemic-induced homebuying frenzy. The median down cost within the second quarter of 2023 was $31,500, based on a report from property information supplier ATTOM, up about 19% from the earlier quarter. Knowledge from the Federal Reserve Financial institution of St. Louis put the median residence sale value for a similar quarter at $418,500.

In a September housing affordability analysis, ATTOM famous that will increase in residence costs and mortgage charges have continued to push bills past what many Individuals earn, sidelining would-be homebuyers nationwide. In additional than half of native actual property markets analyzed, homebuyers wanted annual wages above $75,000 to afford the most important prices related to a median residence.

“The dynamics influencing the U.S. housing market appear to continuously work against everyday Americans,” ATTOM CEO Rob Barber mentioned in a information launch.

Thankfully, there’s no scarcity of applications that may assist cover down payments.

What's down cost help, or DPA?

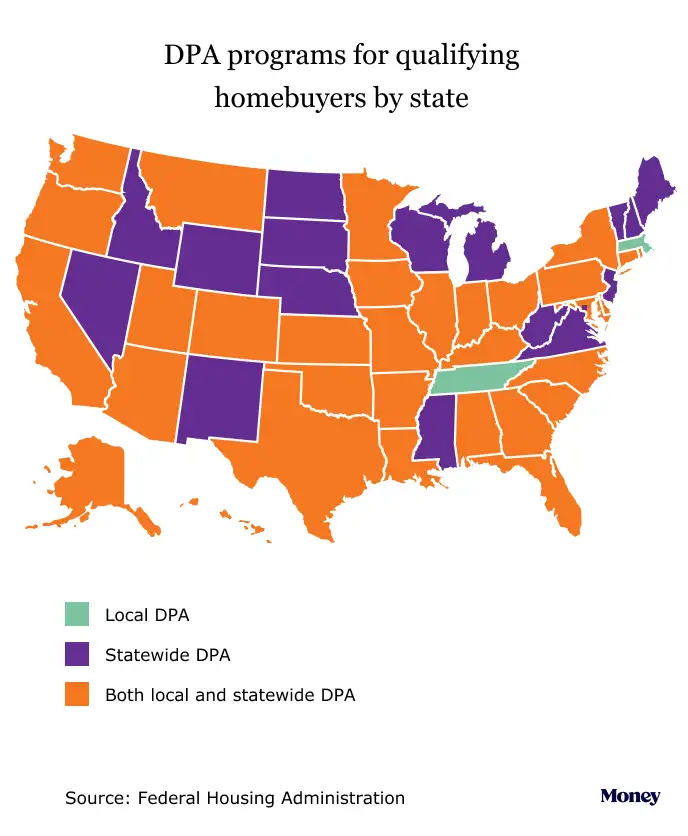

The info within the map beneath is present as of Oct. 10, 2023.

Throughout the U.S., there are greater than 2,000 applications that present down cost help — abbreviated DPA — on the state, regional and native ranges, based on David Berenbaum, deputy assistant secretary for housing counseling on the Division of Housing and City Improvement.

Many of those applications are supplied by way of entities like HUD, state housing finance authorities and municipalities, however there are additionally some led by non-public lenders and group organizations. State and municipal governments typically accomplice with native lenders. Applications are often tailor-made to satisfy the precise wants of homebuyers in every particular person market.

“DPA programs play a critical role to help consumers overcome some of the major challenges in the market right now — one being affordability and the high cost of housing, and the other being interest rates,” Berenbaum tells Cash.

A lot of the DPA applications are solely for first-time residence consumers, based on Berenbaum, whereas about 40% are geared towards different teams, like veterans.

How does down cost help work?

"Help" is, after all, a broad time period. Berenbaum says about 75% of DPA applications provide a money grant for a house buy that can be utilized for down funds and shutting prices. DPA may also come within the type of low- or zero-interest loans, tax credit or forgivable loans.

Loans are offered as a second mortgage and often giant sufficient to cowl your complete down cost. Should you obtain DPA as a forgivable mortgage at 0% curiosity, you do not have to pay it again as long as you reside within the residence for a sure time frame. With a deferred cost mortgage at zero curiosity, you sometimes cannot get forgiveness — however you do not have to repay these loans until you progress, promote your property, refinance your first mortgage or pay it off.

Berenbaum says the quantity of DPA funding an individual can get will depend on the price of housing the place they need to make a purchase order. Some applications and lenders gained’t require any cash down for qualifying homebuyers, whereas others will provide a proportion based mostly on the house’s sale value or present grants as much as a sure greenback quantity, often round $10,000, based on mortgage firm Homebuyer.com.

There aren’t many disadvantages to utilizing DPA applications, based on Berenbaum, though making use of might decelerate the homebuying course of by a couple of weeks. As a result of many applications have residency necessities, they might not be perfect for anybody who expects to maneuver once more inside a couple of years of constructing a purchase order. Furthermore, you often must finance with authorised lenders or merchandise like a Federal Housing Authority mortgage, which is a government-backed mortgage with relaxed monetary necessities.

Learn how to qualify for down cost help

Though these applications are principally out there solely to first-time homebuyers, they sometimes outline a first-time purchaser as anybody who hasn’t owned a house within the final three years. (For essentially the most half, you possibly can’t qualify when you personal rental or funding properties.)

Applications typically have strict earnings limitations that adjust based mostly on location and the price of residing for a specific market, based on Berenbaum, and so they’re often reserved for low- or moderate-income consumers.

“The parameters for a loan in New York state are going to be very different from Colorado or Arizona because New York is one of the most expensive housing markets in the nation,” he says.

Some applications, just like the Texas State Reasonably priced Housing Company’s Properties for Texas Heroes initiative, provide DPA for folks in sure professions, often lecturers, nurses and first responders. Others purpose to develop homeownership for particular demographics, like Black or Latino homebuyers.

Eileen Tu, vp of product improvement for Rocket Mortgage, tells Cash that applications often demand a credit score rating of not less than 620 and constructive credit score historical past. Many additionally require that homebuyers attend coaching workshops or full homebuyer schooling programs to study concerning the mortgage course of and methods to preserve their private funds after making a purchase order.

Learn how to discover a DPA program

Regardless of hovering housing costs lately, Berenbaum says, homeownership remains to be essentially the most cost-effective choice for low- to middle-income Individuals because of the excessive value of rental housing throughout the nation. He advises homebuyers to buy correctly and maintain their minds open.

Each program is completely different, so it’s finest to start out by researching DPA in your state, county and metropolis and reaching out to suppliers with any questions. HUD and the Federal Housing Administration, an company inside HUD, have on-line assets and lists that can assist you seek for applications by location. The corporate Down Cost Useful resource additionally has a database of homebuyer applications and instruments that can assist you decide your eligibility.

Given the variety of homebuyer applications and their distinctive necessities, Berenbaum recommends that homebuyers join with a housing counselor to determine what applications they will qualify for of their area. Each lender has housing counselors out there, he provides, and you'll find counseling by way of HUD.

“Often, we go into a real estate transaction with a lot of preconceptions: 'Where do I want to live? What can I afford? What will be my tax benefit if I do purchase a home?'” he says. “These are all factors that a HUD-approved counselor will help with by developing a budget and setting a range for affordability.”

Counseling may also help with consumers’ post-purchase funds. Berenbaum stresses the significance of sustaining a house and constructing enough “rainy day” assets to keep up homeownership.

The underside line, he says, is that the majority homebuyers stand to profit from DPA applications — so long as they perceive the expectations of the origination and settlement technique of any loans, in addition to the phrases of these loans and their down cost.

Extra from Cash:

How to Save for a Down Payment

Massive Realtor Lawsuit Settlement Will Change How Homes Are Bought and Sold